The Ultimate Month-End Closing Checklist for Finance Teams: A Step-by-Step Guide

Introduction:

When it comes to financial reporting, a smooth and accurate month-end close is non-negotiable. For finance teams, this process plays a pivotal role in ensuring compliance, maintaining data integrity, and empowering business leaders with reliable insights.

However, without a standardized checklist in place, month-end tasks can easily become fragmented, error-prone, and delayed. To help you overcome these challenges, we’ve compiled a comprehensive month-end closing checklist—designed to streamline your workflow and enhance reporting accuracy.

✅ Why Is Month-End Closing So Crucial?

Before diving into the checklist, let’s quickly explore why month-end closing deserves your full attention.

First, it ensures that financial statements are accurate and complete.

Second, it supports compliance with accounting frameworks like GAAP or IFRS.

Third, it offers real-time insights to stakeholders for strategic planning.

Lastly, it allows you to detect and resolve discrepancies early—before they escalate into audit issues.

Now that we understand the importance, let’s walk through each step of a best-in-class month-end closing process.

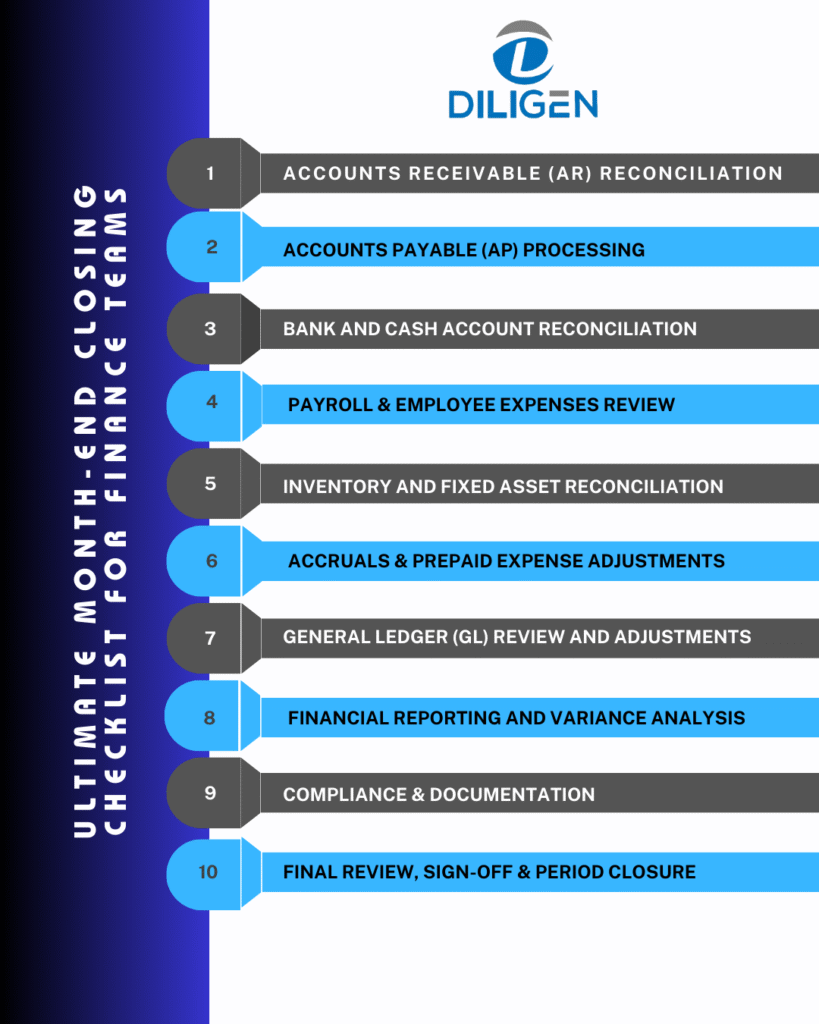

🔹 1. Accounts Receivable (AR) Reconciliation

To begin with, ensure all revenue-related transactions are properly recorded and reconciled.

Key Tasks:

✅ Confirm all customer invoices for the period have been issued

✅ Apply incoming payments to their corresponding invoices

✅ Reconcile the AR sub-ledger with the general ledger

✅ Review aging reports and follow up on overdue receivables

✅ Investigate disputed balances or credit memos

Why it matters: Timely AR reconciliation helps improve cash flow visibility and reduces bad debt risk.

🔹 2. Accounts Payable (AP) Processing

Next, shift your focus to vendor liabilities. Accurately capturing and classifying payables is essential for expense reporting and budgeting.

Key Tasks:

✅ Enter all vendor invoices, including late arrivals

✅ Accrue expenses incurred but not yet billed (e.g., rent, utilities)

✅ Match invoices with purchase orders and receiving reports

✅ Reconcile supplier statements to the AP ledger

✅ Clear any outstanding credits or duplicate entries

Pro Tip: A disciplined AP process prevents misstated liabilities and late payment penalties.

🔹 3. Bank and Cash Account Reconciliation

After addressing receivables and payables, it’s time to reconcile your cash balances.

Key Tasks:

✅ Retrieve bank statements for all active accounts

✅ Match each transaction against general ledger entries

✅ Investigate variances like uncleared deposits or unauthorized charges

✅ Record interest, bank fees, and exchange differences

✅ Reconcile petty cash and credit card statements

Result: This ensures your reported cash position is both accurate and audit-ready.

🔹 4. Payroll & Employee Expenses Review

Subsequently, payroll processing must be reviewed for both accuracy and compliance.

Key Tasks:

✅ Validate payroll runs and post salary journal entries

✅ Reconcile tax withholdings, benefits, and retirement contributions

✅ Approve and record employee expense reimbursements

✅ Accrue unpaid salaries for month-end, if applicable

✅ Allocate costs to appropriate departments or projects

Reminder: Payroll errors can result in regulatory penalties, making this step critical.

🔹 5. Inventory and Fixed Asset Reconciliation

For businesses managing inventory and capital assets, accuracy in asset accounting is vital.

Inventory Tasks:

✅ Perform cycle counts or a full inventory count

✅ Reconcile inventory sub-ledger with the GL

✅ Adjust for shrinkage, spoilage, or obsolescence

✅ Confirm inventory valuation methods are applied consistently

Fixed Asset Tasks:

✅ Record asset acquisitions, disposals, and transfers

✅ Run and post depreciation schedules

✅ Reconcile the fixed asset register with the GL

Efficiency Tip: Barcode systems and inventory management software can reduce manual errors.

🔹 6. Accruals & Prepaid Expense Adjustments

Once your ledgers are clean, focus on period-end cutoffs to reflect expenses in the right period.

Key Tasks:

✅ Post accruals for pending invoices and unbilled services

✅ Amortize prepaid expenses such as rent, insurance, or subscriptions

✅ Reverse stale accruals that are no longer needed

✅ Document all journal entries with appropriate approvals

Insight: Getting accruals right is crucial for accurate profit-and-loss reporting.

🔹 7. General Ledger (GL) Review and Adjustments

Before financial statements can be finalized, your GL must be thoroughly reviewed.

Key Tasks:

✅ Post adjusting journal entries (AJEs) based on findings

✅ Reconcile all sub-ledgers (AR, AP, Payroll, Inventory) to the GL

✅ Review trial balances for anomalies or large variances

✅ Validate intercompany eliminations and transfers

✅ Substantiate key balance sheet accounts with supporting documents

Best Practice: Implement a materiality threshold to prioritize reviews effectively.

🔹 8. Financial Reporting and Variance Analysis

With reconciliations complete, you can now move into the reporting phase.

Key Tasks:

✅ Generate preliminary financial reports: P&L, Balance Sheet, and Cash Flow

✅ Analyze budget vs. actuals and highlight major variances

✅ Create dashboards or management summaries with actionable insights

✅ Finalize reports and distribute them to decision-makers

Tech Tip: Leverage tools like Power BI, Tableau, or Excel pivot tables for visual clarity.

🔹 9. Compliance & Documentation

Proper documentation not only ensures transparency—it also protects you during audits.

Key Tasks:

✅ Store supporting documents: invoices, approvals, reconciliations

✅ Ensure compliance with accounting standards (GAAP/IFRS/local)

✅ Prepare audit schedules and working papers

✅ Centralize your files using cloud-based document management tools

✅ Maintain an audit trail for all journal entries and changes

Reminder: What’s not documented is as good as not done.

🔹 10. Final Review, Sign-Off & Period Closure

Finally, conclude the process with a formal review and secure closure of the books.

Key Tasks:

✅ Review the entire checklist with the Controller or CFO

✅ Obtain approvals from department heads or senior management

✅ Lock the accounting period in your ERP system to prevent backdating

✅ Communicate closure to relevant teams

✅ Roll forward recurring entries and prep for the next month

Closing Tip: Always hold a post-close review to capture lessons learned and process improvements.

🧩 Best Practices for a Streamlined Month-End Close

To summarize, here are several best practices that can drastically improve your month-end cycle:

- 📅 Set up a shared closing calendar with task owners and deadlines

- 🔄 Automate repetitive tasks like reconciliations and invoice processing

- 📋 Standardize your SOPs and use checklist templates

- 👨🏫 Train your team on new systems, standards, and workflows

- 🔍 Conduct monthly close reviews to improve speed and accuracy

✅ Conclusion:

Close with Confidence—Partner with the Best

Month-end closing doesn’t have to be stressful or chaotic. With the right checklist, tools, and workflows in place, your finance team can close the books quickly, accurately, and with full compliance.

However, if you want to elevate your financial close process to the next level—minimizing risk, improving efficiency, and gaining deeper insights—partnering with experts makes all the difference.

👉 Diligen’s professional experts are the best in the market, offering end-to-end support for your month-end, quarter-end, and year-end close processes. From reconciliations to reporting and compliance, we bring unmatched expertise, precision, and reliability to every engagement.